Sales forecasting

and inventory optimization

Become a retail mastermind you always wanted to be.

Become a retail mastermind you always wanted to be.

By: Jul Domingo

Retail companies are vulnerable to two issues: economic woes and inefficient internal processes. These stumbling blocks have made business ownership harder for 72% of entrepreneurs.

But unlike economic issues, you can do something to rectify internal inefficiency. Your process is something you can control. To ensure your retail store survives hard times, run health checks on a regular basis and implement new strategies to counter problems as they emerge.

Retailing is never easy, but the right practices can help you face future risks. Coupled with the right tools, it’s possible to transform your business and make it leaner.

Take the time to educate yourself and your team about the current retail problems and solutions. We’ve outlined a few below.

Retail businesses—both start-ups and growing companies—need to take proactive measures to remain competitive. But you need to be smart about it since your resources are limited.

Learn how to avoid business failure with these suggested solutions (even if you haven’t encountered some of these issues yet).

Running a retail business means focusing on customer service, demand fulfillment, sales promotions, and inventory management. Mapping out plans in these areas needs solid, reliable data.

Biased, gut-driven decisions are common when a company has no single source of truth. It’s easier and common (over 58% of survey respondents) to “trust your instincts” because, well, you don’t have other things to rely on. But this has repercussions.

For instance, without knowing how much profit your brick-and-mortar stores and online platforms make, it’s possible to believe that you’re making money even when one of your channels is underperforming. This lack of data can further influence ill-informed initiatives, such as continuously stocking up on underperforming products.

Define your short and long-term goals and find the right tools for capturing, storing, and interpreting relevant data. Data you can use to create better, more effective strategies.

If you’re looking to optimize your website, simple and free tools, like Google Analytics, exist, so you can monitor visitor behavior and find out where you need to improve.

Advanced data and analytics tools, on the other hand, can detect patterns to assess past performance and understand future events.

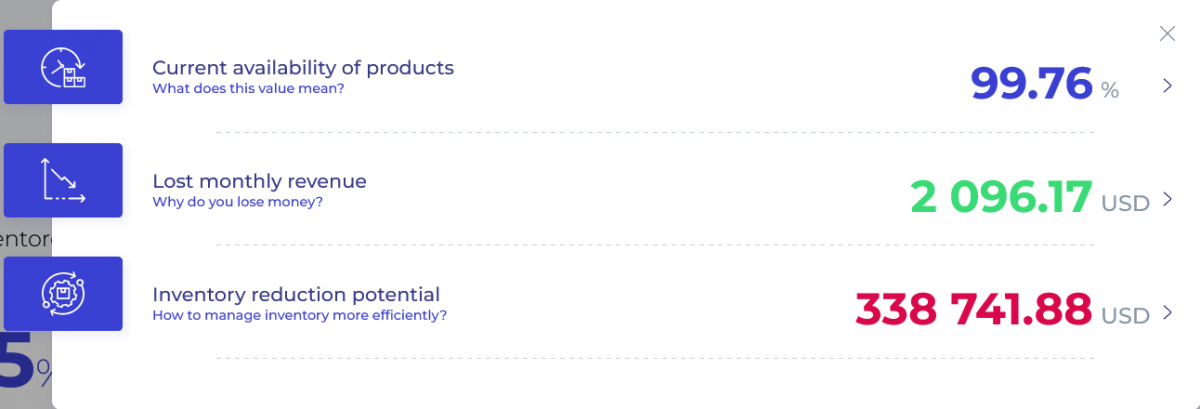

For instance, Inventoro’s sales forecasting tool uses mathematical equations and deep machine learning to maximize your investment across all of your warehouses and sales channels. It all depends on your strategy.

Kulina, a decade-old store, doesn’t take any chances. The company uses quarterly goals to drive its sales forecasts. Keeping ahead of the game allows them to develop favorable relationships with their suppliers through strategic bulk buying.

With our tool’s Golden Brick feature, the brand can also see how much money they lose by not selling certain items. Seeing their potential, they can find out which products are worth investing in. Read more about our case study here.

The bottom line? Data-based insights and forecasts allow businesses to optimize their performance by addressing gaps before they turn into nightmare scenarios. Rather than making wild guesses from thin air, data enables your business to make informed, reliable decisions.

Some retail businesses put their eggs in multiple baskets without optimizing their selling channels and product portfolio.

Approximately 63% of customers expect businesses to know their unique needs (e.g., product availability, price fairness, convenience, and timely fulfillment). Otherwise, the unmet expectations may leave them feeling disappointed and unsatisfied.

As an example: Dressbarn, a women’s clothing retailer, incurred losses when it closed all 650 retail outlets in 2019. Due to online shopping’s popularity, it was unable to attract foot traffic. It’s a waste of resources if you stocked too many products at each of your retail outlets when your customers mostly shop online.

In the same vein, if you continue to invest in the wrong products, you may find yourself–even facing a double trouble situation. Your shop will constantly run out of popular items, which might cause 70% of your customers to switch to your competitors.

You’ll also pile up your warehouse with permanent occupants. And the more dead stock there is, the higher the holding costs. This ceramic business case study proved that the product cost to a company is more than production costs alone. The accumulated warehouse, maintenance, and disposal expenses play a huge part.

Over time, your stocks will skyrocket without meeting demand, creating a fertile ground for retail failures.

Conduct research about your products and channels through reviews, surveys, and direct interviews. To do so, reassess the customer journey from the initial touchpoint to the point of purchase, then decide when to bring your chosen medium in.

If you decide to go for a survey, you can sneakily add a pop-up feedback form or a separate contact page like this one from Supernatural, a retailer of plant-based food products.

Source: Supernatural

Customer feedback can help improve key areas where customer satisfaction falls short. It could be the quality, the price, the product availability, or the payment method.

You can also gain an in-depth understanding of demand with a product portfolio tool like Inventoro. It lets you stock up on in-demand items while removing those with the lowest turnover rate.

About 21% of retailers are reducing their portfolio and focusing only on a few products for the same reason. It allows them to nurture their top-selling products while preventing lost sales opportunities.

Understanding these market-related retail problems and solutions can sustain your business, especially during an economic downturn.

Some retail businesses put their eggs in multiple baskets without optimizing their selling channels and product portfolio.

Approximately 63% of customers expect businesses to know their unique needs (e.g., product availability, price fairness, convenience, and timely fulfillment). Otherwise, the unmet expectations may leave them feeling disappointed and unsatisfied.

As an example: Dressbarn, a women’s clothing retailer, incurred losses when it closed all 650 retail outlets in 2019. Due to online shopping’s popularity, it was unable to attract foot traffic. It’s a waste of resources if you stocked too many products at each of your retail outlets when your customers mostly shop online.

In the same vein, if you continue to invest in the wrong products, you may find yourself–even facing a double trouble situation. Your shop will constantly run out of popular items, which might cause 70% of your customers to switch to your competitors.

You’ll also pile up your warehouse with permanent occupants. And the more dead stock there is, the higher the holding costs. This case study of a ceramic company shows that the product cost to a company is more than production costs alone. The accumulated warehouse, maintenance, and disposal expenses play a huge part.

Over time, your stocks will skyrocket without satisfying the demand—this makes for a fertile ground for retail failures.

Conduct research about your products and channels through reviews, surveys, and direct interviews. To do so, reassess the customer journey from the initial touchpoint to the point of purchase, then decide when to bring your chosen medium in.

If you decide to go for a survey, you can sneakily add a pop-up feedback form or a separate contact page like this one from Supernatural, a retailer of plant-based food products.

Source: Supernatural

Customer feedback can help improve key areas where customer satisfaction falls short. It could be the quality, the price, the product availability, or the payment method.

You can also gain an in-depth understanding of demand with a product portfolio tool like Inventoro. It lets you stock up on in-demand items while removing those with the lowest turnover rate.

About 21% of retailers are reducing their portfolio and focusing only on a few products for the same reason. It allows them to nurture their top-selling products while preventing lost sales opportunities.

Understanding these market-related retail problems and solutions can sustain your business, especially during an economic downturn.

Most retail problems and solutions revolve around inventory, as it is a retailer’s most significant investment.

Poor inventory practices can suck up your capital, cause store inefficiencies, and make you lose your competitive edge. Moreover, not replenishing on time or selling as fast as you forecasted can also lead to significant financial losses.

McKinsey reported that 32% of businesses blamed their supply chain woes on inventory inefficiencies, such as poor forecasting and demand variability. In a separate study, ineffective replenishment methods are reported to account for 70% to 90% of out-of-stock situations. Your retail business is likely to suffer without strategic management to resolve these issues.

Address the root of inventory problems by observing irregularities in the process flow. Do you often struggle with overstocking or stockouts? Is your inventory costing you too much and turning over too slowly? Perhaps, your Excel forecast calculations don’t bring accurate results.

If that’s the case, conduct an inventory audit on a separate record to correct any incorrect balances. Don’t forget to double-check the count of your recent purchase orders as you reset your stock balances. For better results, you can invest in sales forecasting and intelligent replenishment tools to reduce human intervention and errors in the long run. It’ll also save you up to 20 hours a week on mundane admin tasks.

Retailers need to rethink the way they manage their stocks. About 77% of business owners already responded to that call by using technology to upgrade their inventory management.

All things considered, manual inventory management is no longer the most efficient way to keep track of all the inventory going in and out of your business. While paper based methods are used by many small businesses, in order to scale up you will need to implement more universal inventory management systems that allow you to oversee inventory throughout large warehouses or across multiple locations.

Some short-term cash flow problems can cause long-term insufficiency in your operating capital. After all, it wouldn’t be possible for your business to function without cash. 82% of failed small businesses point to poor cash flow management as the reason for their demise.

The temporary lack of cash on hand can also accumulate unpaid bills and invoices inflated by interests and penalties.

Worse, this breach of contract can also prompt legal action, causing irreversible damage to your business.

How do you avoid business failure caused by negligent cash flow management? It’s a simple money rule: don’t let your outflows exceed your inflows.

However, that’s not always feasible as sales fluctuate, and some customers settle their invoices late.

So, it’s pivotal to identify the factors affecting your poor cash flow and implement strategies to alleviate the problem.

Slow receivable collections? Try offering early payment incentives. Low sales or poor inventory turnover? You can devise new marketing efforts and increase your cash flow by bundling your products or holding flash sales.

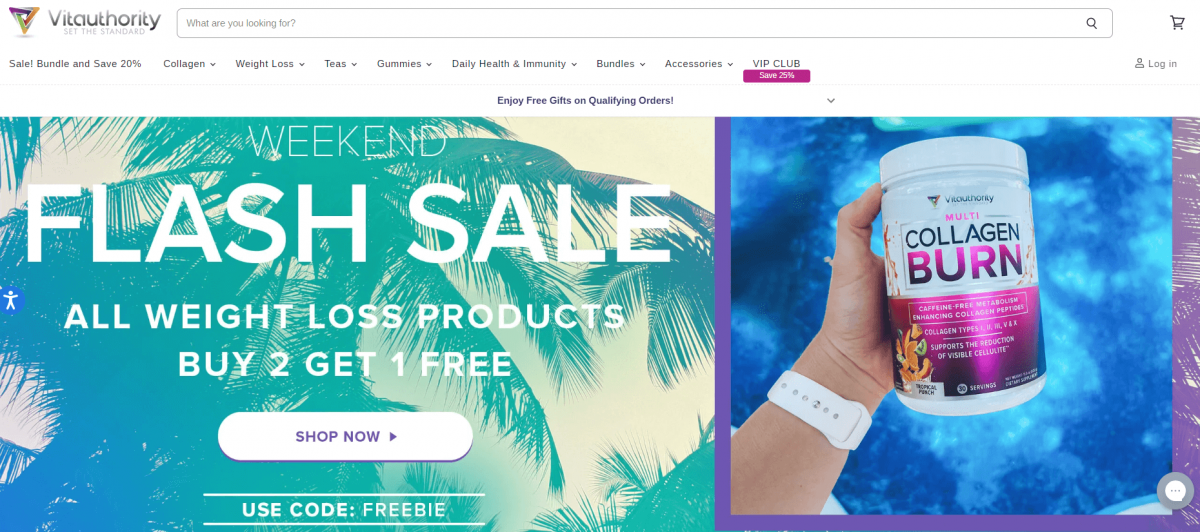

Source: Milled

Take a cue from Vitauthority, an online supplement provider. Pair your slow-moving products with your bestsellers. This strategy is two-fold. First, it reduces your inventory holding costs lowering your outflow. Second, sold bundles boost your inflow.

Source: Vitauthorithy.com

Another strategy you can borrow from the online brand is holding flash sales. But make sure you do this in moderation to avoid reducing the value of your brand and your products.

Read about cash-flow-related retail problems and solutions in this article.

Retailers who don’t collect feedback or act on one are likely to develop toxic customer relationships.

Customers are the sole reason your business exists. Poor customer service and under-delivered promises can drive potential customers away and hurt your brand reputation. This is likely due to the staggering 62% of past shoppers who admitted sharing negative experiences with others (who might be your prospects).

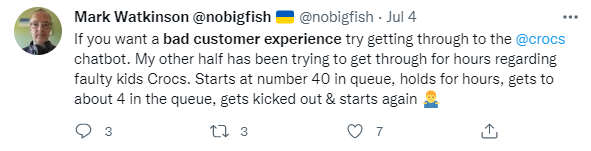

Most of these customers will take to social media to vent their frustrations. And when it hits the socials, who knows how far it will go. TikTok videos with #badcustomerservice have garnered about 73 million views.

Meanwhile, on Twitter, it’s common to call out companies and tag their accounts. Which is exactly what this unhappy Crocs shopper did:

Source: Twitter

Listen and respond to customer requests promptly and be transparent with them. You can involve in-store customers by displaying suggestion boxes in your outlets and training staff members on how to cater to your shop visitors better.

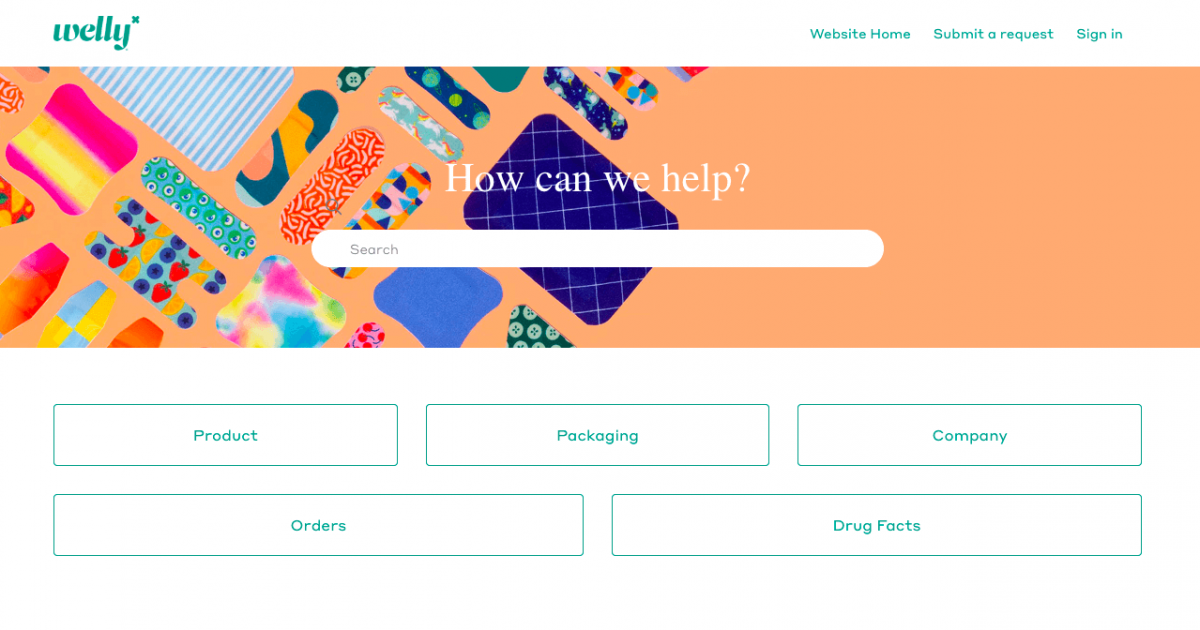

Online, you can include a FAQs help center and a request form on your website, like this one from Welly, a first aid kit retailer. You don’t have shop attendants that can help your customer navigate through your online store, so it’s a good idea to anticipate what they’ll need and hand it to them before they ask.

Source: Welly

Last but not least, make a difference in customer experience–both online and offline–by satisfying your customers with a broader product range. They won’t have to ditch you for competitors like the 61% of buyers who would switch to a new brand after a poor shopping experience. Use the right tool to achieve it with minimal inventory investments.

Excellent customer service leads to three times higher returns and faster financial recovery for retail businesses. You’ll do well to hone your business in this area. Pro Tip: By automating repetitive business tasks, you can devote more time to customer service.

PPC advertising is a retail game-changer. About 19% of people click on paid ads because of a compelling title, description, or image—imagine the traffic and engagement you could garner. However, focusing on fleeting pay-per-click ads alone can only build awareness and not long-term customer loyalty.

General retail and online retail businesses experience 24% and 22% customer churn rate, respectively. Your advertisements may be effective at attracting prospects. But your business can’t grow unless you encourage existing customers to return.

Let’s recall the first talking point on this list of retail problems and solutions: back up your digital marketing efforts with customer data and analytics.

With richer and more accurate insights, you can tailor your brand promotions to their preferences and behaviors.

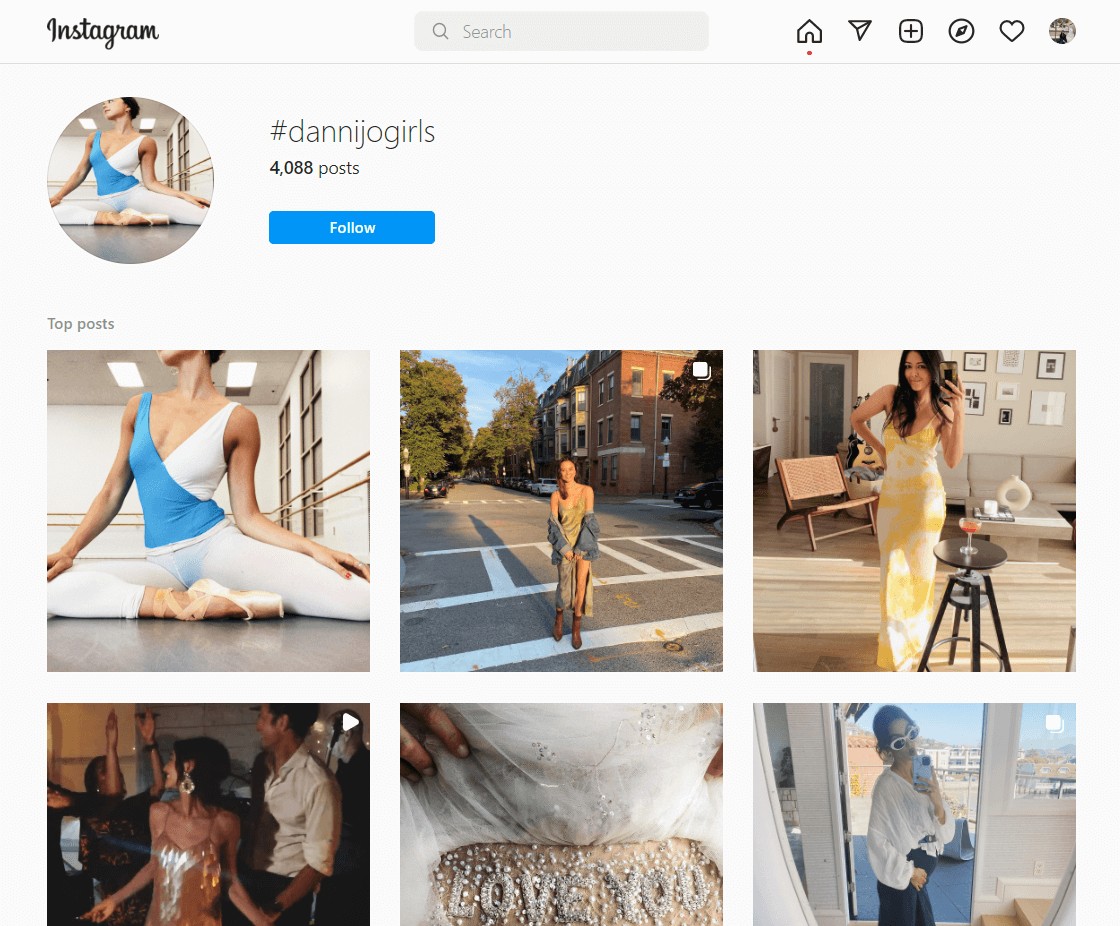

Show off your unique brand voice and story with visual content your customers would really want to see. Look at how Dannijo markets itself as a sisterhood, and not just a jewelry brand.

The #DANNIJOGIRLS hashtag used by the community is also a clever way to improve searchability, impressions, and engagements.

Source: Instagram – Dannijo

Other strategies include introducing loyalty programs, rewards, and discount vouchers for their next purchases. You can also throw gifts into every order exceeding a certain amount. This is a clever way to dispose of dead stock in your warehouse while demonstrating generosity to your shoppers. Find out how to get rid of dead stocks here.

The goal is to nurture each lead through the following stages: reach, acquisition, conversion, retention, and loyalty. If you do this right, you can attract 80% of customers who believe that being loyal to a brand involves frequently purchasing their products.

Growing your business has two major goals: remain competitive and remain relevant.

Complacency can lead to retail failures. If an emerging retailer with breakeven sales is no longer willing to take on additional risks to enter new markets, there’s little choice but to scale back to survive.

It’s even happened to large enterprises. We’ve seen Fortune 500 companies go under this way (Blockbuster, General Motors, Kodak, and Toys R Us), proving that a progressive approach is essential to success.

But even if you sell innovative products and keep up with the trends, it’s not enough. You need to encourage customers to come back.

Unfortunately, this was revealed late to the DTC mattress brand Casper. What was once a fast-growing company found itself in a bind after realizing that it didn’t offer any significant benefits to its existing customers.

Of this list of retail problems and solutions, this one offers varying solutions. It all depends on your plan.

Remaining competitive requires a straightforward approach: Adapt to trends–whichever way it looks for your competitors.

Understand demand and economic fluctuations, and assess how you can modify your offers to gain a competitive edge. Then, use these insights to outperform your competitors and boost customer trust.

Next is to research your company’s strengths, weaknesses, opportunities, and threats in the industry.

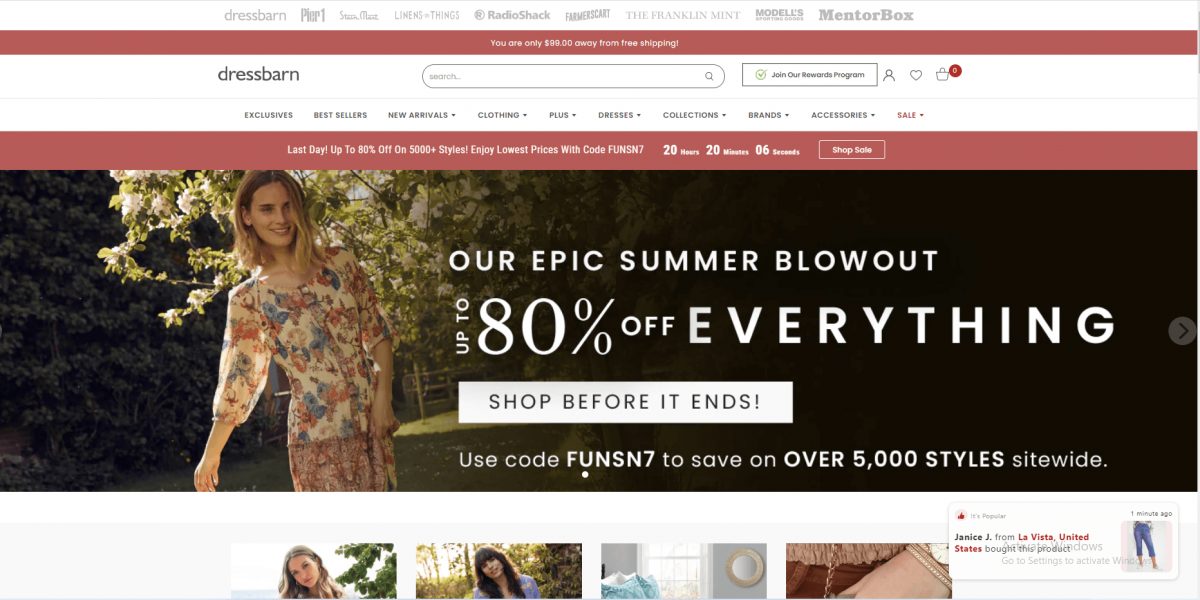

Dressbarn now operates as an online retailer. Source: Dressbarn.com

After the demise of Dressbarn, a new parent company brought it back to life by converting it into an online retail store and capitalizing on the surge in e-commerce sales. Good news: the fashion retailer continues to thrive today.

Being competitive is part of remaining relevant. But a large chunk of it is cultivating strong business relationships as a foundation for growth. Engage and build trust with both your suppliers and customers.

For suppliers, long-term partnerships are key. This study proves that your suppliers would want a lasting relationship with you. They win by having lower selling, general, and administrative expenses.

You win by negotiating a better, long-term deal. We’ve seen this happen to our customers. Our “merge orders” function can help them gauge how much they’ll need from their suppliers. They leverage this information by getting a sweeter but more lasting contract.

As for building trust with customers, serving them better often works. The tips in items #2, #3, #5, and #6 provide some helpful advice.

If scaling up for growth is essential, so is proper timing. Premature scaling practices aren’t only expensive and can end your retail business for good. According to this IBFR study, a lack of business plan is a major culprit for startup and scaling business failures.

Such as the case with Wise Acre Frozen Treats when it landed a contract with a national distributor without enough resources.

CEO Jim Picariello applied for several loans to fund the massive increase in demand. Yet despite ongoing efforts to scout bankers and investors, they’re still unable to raise the money necessary to pay the bills and continue the operation. In the end, this poor timing resulted in thousands of unfulfilled orders and a bankruptcy filing.

Expansion is any business owner’s point of no return. It’s not for the fickle-minded. So, before signing any contract and applying for bank loans, ask yourself these questions first:

Once you’re confident, document the new business processes and take the time to onboard your staff. Then, you have all the time to equip yourself and your team to review these retail problems and solutions.

10. Lack of task delegation

Retailers, particularly small business owners, tend to avoid hiring more workers to reduce costs. It’s not discouraged, but the problem arises when a lack of task delegation begins to burn you and your existing team. Stress and burnout remained high for managers, and it could only get worse without proper task delegation.

Work-related burnout reduces professional efficacy and compromises the quality of work, which can be just as costly as outsourcing. Taking on even the smallest routine tasks as an entrepreneur is no different.

You can delegate tasks through third-party outsourcing if you can’t afford to hire full-time retail employees. Look for freelancers and agencies who can assist you fulfill time-consuming tasks, such as social media and content marketing, repetitive administrative tasks, warehousing, and order fulfillment.

For instance, outsourcing logistic services from 3PL providers can save you the hassle of paperwork and frequent audits. Even better, they can help reduce shipping errors, delayed shipments, and stockout situations–especially if you’re making the move to micro-fulfillment, a growing trend in retail.

Using this distribution method, the fulfillment facility is localized near the customer base, thus shortening delivery lead times.

To help you determine which businesses are likely to benefit from this, Nick Malinowski, co-owner of 3PL company OTW Shipping LLC, explained: “Micro-fulfillment is going to be crucial for large retailers to offer an improved delivery experience for impatient customers. It also opens up the option for grocery delivery.”

Your staff will have a lot to do if you decide this model is right for your business and customers. You’ll also have to shell out resources (time and money) to get it done. Outsourcing takes away the hurdle and makes it easy to dive in and try things out without taking a huge financial hit.

No business has ever succeeded without first facing risks and challenges. Confront them confidently by relying on data, fulfilling demand, optimizing processes, boosting capital, and staying one step ahead of the competition.

With Inventoro’s smart inventory features, you can achieve all of the above on your most valuable asset: inventory. Use it to optimize your product portfolio, generate accurate sales forecasts, and receive daily replenishments to maintain your stocks at optimal levels.

Request a demo today.

Become a retail mastermind you always wanted to be.